From the IMF's Regional Economic Outlook: Asia and Pacific:

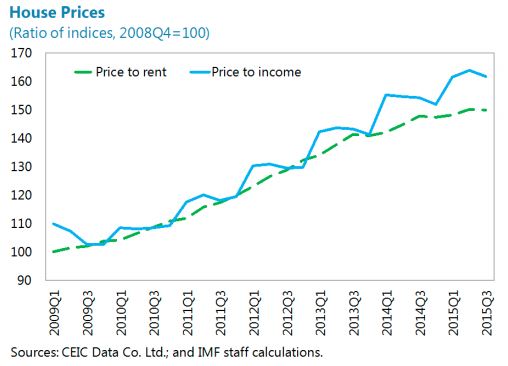

House prices in Australia and New Zealand have more than doubled in real terms since 1990, rising substantially faster than the Organisation for Economic Co-operation and Development (OECD) average (Figure 1.1.1). This increase has often been attributed to the liberalization of their banking systems during the 1980–90s and the transition to lower interest rates in the last decade (see Hunt 2015; Ellis 2005). The rise in house prices has been accompanied by a sharp increase in household debt, with debt-to-income ratios roughly tripling since the 1990s in both countries and mortgage debt accounting for a substantial share of the total. Household debt-to-income ratio is a key variable from a financial stability and macroeconomic risk perspective as it reflects the risks borne by households and the possible amplification of house price declines to the macro economy (Debelle 2004; April 2014 Regional Economic Outlook: Asia and Pacific, Chapter 2).

The housing market in both Australia and New Zealand appears to reflect moderate overvaluation. Valuation ratios such as price to income are now above historical norms. While some of that is expected given low interest rates (allowing higher debt to be serviceable), other fundamental factors such as income per capita, interest rates, and working-age population suggest moderate overvaluation (see IMF 2015a, 2016c). The financial stability heat map also suggests that prices are currently higher than recent trends (Figure 1.13).

Concerns about house price inflation have been prominent for well over a decade and have triggered regulatory and prudential responses. Recently, the authorities in both countries have stepped up measures. In October 2013, the Reserve Bank of New Zealand (RBNZ) placed a temporary “speed limit” on high loan-to-value ratio (LVR) residential mortgage lending, whereby banks must restrict new mortgages at LVRs more than 80 percent to no more than 10 percent of their total residential mortgage lending. Although house price inflation in Auckland initially moderated in response to the measures (and tighter monetary policy), it has subsequently accelerated. In May 2015, the RBNZ announced additional measures (effective November 2015): (1) residential property investors (though not owner-occupiers) in Auckland are required to have a deposit of at least 30 percent; (2) the existing 10 percent speed limit for loans at high LVRs is retained in Auckland, while it is increased elsewhere to 15 percent to reflect the more subdued housing market conditions there; (3) a new class for loans to residential property investors was established and expected to attract a higher risk weighting than owner-occupier mortgages; (4) the 2015/16 budget introduced a new property sales tax for nonprimary residences that are bought and sold within two years; and (5) the government announced a tightening of reporting and taxation rules for foreign buyers.

The Australian Prudential Regulatory Authority (APRA) has stepped up its supervisory intensity through a gradual and targeted approach. It advised banks in December 2014 that it would focus on higher-risk mortgage lending (interest-only and high loan-to-income or loan-to-value ratios), issuing guidelines to limit growth of investor lending to 10 percent a year, and strengthening loan affordability. In response to the recommendations of the Financial Sector Inquiry, APRA announced that large banks would need to hold more capital against residential mortgage exposures by raising the average risk weight (to 25 percent) for large banks. Recent data suggest that house price inflation is gradually responding to the regulatory measures, but it is too early to assess whether such inflation is at more sustainable rates.

Can the banking sector withstand a housing downturn? Four large Australian-owned banks account for the bulk of banking sector assets in both Australia and New Zealand. Against this background, the authorities in both countries have collaborated on stress testing, including a combined scenario with a severe downturn in the housing market (40 percent cumulative decline) (APRA 2014). While this extreme scenario would have a substantial adverse impact on profitability and capital ratios, with losses on residential mortgages accounting for about one-third of total credit losses, minimum capital requirements are not breached. However, banks with substantially reduced capital ratios would be constrained in their ability to raise funding, impacting credit growth and aggregate demand.

"Household debt has increased by 15 percentage points of GDP since end-2009 but growth has begun to moderate as of late (...). Close to 50 percent of the debt is owed on residential property and about 60 percent are variable rate loans. Macroprudential measures have helped to curb household borrowing (...). The impact of measures continues to be felt and the reduced loan applications and approvals reflect in part an enhanced framework for risk-based pricing of loans. Risks from high household debt are mitigated by strong household financial assets (...) and low unemployment. NPLs are likely to increase as the financial cycle turns but any increase is likely to be small. House prices are still growing but prices of highend properties in Kuala Lumpur have declined slightly. Given the slowdown in loan growth and in housing, no further measures are recommended. LTV caps on second and first mortgages should be considered if rapid house price and credit growth were to reignite", according to the IMF's latest report on Malaysia.

"(...) since the crisis, estimates based on the MVF2 [the multivariate filter with financial frictions] have been higher than those by other methods, suggesting that house prices and credit have been particularly low relative to potential levels," according to IMF's report on Hungary.

Turns in the economy take economists, even the best of them, by surprise. In late-August 1990, Alan Greenspan, then chairman of the Federal Reserve, said that “those who argue that we are already in a recession are reasonably certain to be wrong”—of course, the recession had already begun. His successor, Ben Bernanke, predicted in 2007 that the “subprime problem [in the housing sector] is contained.” Yet, without forecasts, as this excellent new report from the World Economic Forum notes, we would be driving a car “while looking only in the rear view mirror rather than through the windscreen.”

There are few economic forecasts more important than those of the real estate sector. As Ed Leamer has said, “housing is the cycle.” Collapses in this sector have been associated with severe crises, including the global financial crises of recent years. While this crisis increased the spotlight on the residential sector, much less is known about the commercial real estate sector.

This report is thus welcome for the information it provides on the commercial real estate ecosystem—the main players and their motives. But the report is far more ambitious. Its goal is to provide an early warning system for commercial real estate crashes. Moreover, the intent is to build a system that can be scaled up to the global level—it is currently applied to 10 U.S. cities— and also applied to other asset classes, including the residential real estate sector.

So, does the effort succeed? Yes, in my view. The authors show that the risk of crashes in the commercial real estate prices in U.S. cities can be linked to developments in a few macroeconomic indicators—inflation rates, bond yields, consumer confidence, employment—and to growth in the sector’s net operating income. There is thus no complex or secret ingredient needed to assess the risks of crashes: one only has to look out the windscreen.

This is a useful exercise even if, as the authors readily admit, they do not try to understand the deep causes of what leads sharp run-ups in commercial real estate prices in the first place. As they note, often “one does not need to know the causes of a condition to be able to diagnose the effects of the condition.” Academics may have the luxury of debating what causes ‘bubbles’ in real estate markets—or indeed if they even exist—but policymakers have to deal with the consequences of cleaning up the mess when there is a crash, regardless of why it happened. Whether there was a bubble in house prices in Ireland in the 2000s will be the topic of numerous doctoral dissertations; what the policymaker takes from episode is that the cost of cleaning up after the crash was 40 percent of the country’s annual income.

The IMF is happy to have been part of the advisory and steering committee that has guided this report and the other important work carried out by the World Economic Forum’s Asset Dynamics group. We share the desire to pay close attention to the real estate sector, to devise policies to ward off crashes, and to put in place policies that will minimize the costs of crashes that will nevertheless occur. As our Deputy Managing Director Min Zhu declared in 2014, “the era of benign neglect of house price booms is over.” I look forward to the extension of the early warning system developed here to other cities and to sectors, including residential real estate.

My talk to parliamentarians from around the globe. Yes, (the Bank-Fund) Spring (Meeting) has sprung.

From the Global Housing Watch Newsletter: March 2016

In the interview below, Marja C Hoek-Smit—Director of the International Housing Finance Program at the Wharton School and Director of HOFINET—the Housing Finance Information Portal—talks about her work, about housing markets in emerging and developing economies, and about some of the challenges, and success stories. In doing so, she provides a global picture of the housing market in emerging and developing economies—a region where much remains to be known.

Hites Ahir: Please tell us about your work.

Marja C Hoek-Smit: The broad focus of my work is first on improving the efficiency and reach of urban housing markets in developing and emerging market countries, both real-side markets and housing finance markets. Second, an increasingly important part of what I do is to find the best way to subsidize those who cannot afford to pay for available housing or need a subsidy to access housing finance. In many emerging market countries 60 to 75 percent of the urban population cannot access formal housing markets for a variety of reasons.

Housing is important from an economic, social and political perspective, and, in countries with substantial mortgage markets, the housing sector is critical from a financial stability perspective. Yet, housing has for the past decades not received the attention it deserves, and housing conditions in some developing countries have deteriorated despite economic growth. International agencies have mostly focused on upgrading slum areas. Poor housing is too often just seen as a poverty or low-income problem relative to “unavoidable” house-price trends, a perception that leads to very blunt policies for the improvement of housing conditions, in particular in the type of subsidies applied to housing. For example, in many countries subsidizing interest rates on mortgage loans provided through state housing finance institutions, remains the preferred way to address the “affordability” problem, even though such subsidies are known to be unnecessarily costly, limit the expansion of the private housing finance system and are inequitable. Reasons for high and increasing house-prices are often not analyzed in any detail, nor are reasons for housing finance markets to remain small and mortgage interest rates high relative to the risk-free rate. Yet answers to these questions are critical in the design of the right policy instruments aimed at making these systems more efficient.

Housing markets are complex and depend on well-functioning finance- and land-markets, and on facilitative legal and regulatory systems and administrative procedures in these supply markets. The analysis of housing markets therefore requires many different types of skills. In many countries housing policy is still seen as the domain of planners and architects, and it is difficult to incorporate economic and financial sector aspects of housing in policy analysis.

My consulting work is focused on assisting governments in bringing the different strands of housing market analysis together- on the demand and supply side- and in developing comprehensive housing policies for different segments of the housing market. For the broad middle income market that means addressing the constraints facing private developers in supplying housing for this population segment, and working with the financial sector to assist the expansion of mortgage markets. Relatively small demand-side subsidies may be needed to improve access for households at the margin. For the market segment where low-incomes and poverty make it impossible for market actors to deliver housing, support needs to be much more comprehensive and may focus primarily on the supply of rental housing or alternative home-ownership strategies.

The second pillar of my work is education. My academic and executive teaching is similarly focused on the housing sector in this broader context. Jointly with my colleagues from the Wharton School, I established an executive education program with a focus on housing markets, and housing finance sector analysis, and the related public policies, for senior public and private sector professionals from developing and emerging market countries. The International Housing Finance Program (IHFP) of the Wharton Zell/Lurie Real Estate Center has consistently offered courses both at Wharton and in emerging market countries over the past 30 years and has developed a joint housing finance program for Sub-Saharan African countries with Cape Town University.

More recently a third component has been added to this mix, the development of global data systems for the housing finance sector. Because of the dearth of comparable data on housing markets and housing finance systems globally, the IHFP established a standardized and longitudinal data collection effort – the Housing Finance Information Network. We research and work with many countries’ housing finance institutions to collect such data for more than 140 countries and make it available on a public web-portal -- HOFINET. http://hofinet.org

Hites Ahir: What are the key problems and challenges that the housing sector faces in emerging market economies?

Marja C Hoek-Smit: On the demand side, low incomes relative to house prices, the informality of incomes (often as high as 60 percent of the labor force), high inequality (increased over the past years particularly in Sub-Saharan Africa and SE Asia), high indebtedness, and related low propensity to save, are major constraints on the demand side, exacerbated by a lack of access to finance.

On the supply-side, constraints in real-supply-systems are frequently a more difficult problem to solve and lead to high prices relative to construction costs. Rapid urbanization at increasingly lower levels of per capita income strain governments’ capacity to provide services and infrastructure, including transportation systems, for formal housing expansion, increasing land scarcity. Unrealistically high standards and zoning/planning restrictions, as well as inefficiencies of the permitting process drive up housing costs and make it impossible for developers to cater to lower middle, and middle income groups.

Difficulties in safely expanding housing finance systems, are often a more binding constraint on the supply-side and include: i) poor systems to understand and deal with credit risk, ii) high transaction costs associated with lower-income and non-salaried customers, iii) stress on funding sources, iv) lack of mechanisms to deal with asset-liability mismatches when capital market funding is limited, and, iv) in some emerging market economies, the dominance of government housing finance systems benefitting from implicit subsidies and the related reluctance of private lenders to enter the market, ultimately limiting the overall scale of mortgage availability. In addition, Basel III regulations and solvency and liquidity requirements make it more difficult for the banking sector to expand longer term mortgage lending and the banking sector is the core provider of mortgage loans in most emerging market countries.

Hites Ahir: Which regions face the biggest challenges and why?

Marja C Hoek-Smit: Low-income countries that are urbanizing rapidly, starting from a low urban base, face the most complex urban housing problems, i.e., countries in Sub-Sahara Africa, and South and SE Asia. On the other end of the spectrum are the highly urbanized middle income countries of Latin America with dominant state supported and subsidized housing finance systems, such as Mexico and Brazil, which have created policy-induced volatility in the housing- and construction markets and stress in the housing finance systems. While these policies were successful in addressing high income inequality, they created locational inequalities and housing risks for households and government. Mexico has started a process of comprehensive policy reform both on the real-supply side and in the housing finance system.

Hites Ahir: What are some of the successful approaches to expand affordable housing?

Marja C Hoek-Smit: From the above discussion it follows that there is not one right approach or set of policies that address the housing affordability problems across emerging market countries and that policies must differ according to the specific demand and supply constraints in each market. In general, countries that have invested in a comprehensive housing market analysis, differentiated by type of urban area, and have put in place a medium/long-term agenda for reforms of land-policies, and land registration systems, planning regulations, housing finance sector and subsidy policies, have done better compared to countries with similar demographics and income levels that have not addressed these issues. Several countries are in the process of implementing such comprehensive approach to housing reforms, e.g., Mexico, South Africa, Egypt, India, and, although in an early phase, Indonesia. I focus here on two countries that have gone through such reforms in the past.

Thailand is a country that reformed its housing finance system and its urban development policies in the 1980s and 1990s, and was able to gradually expand the formal supply of middle and lower-middle income housing with minimum subsides. Community-based upgrading and resettlement policies were effective in further decreasing its sizable urban slum population by the early 2000s. Political instability and budget cuts for housing during the recent decade, however, are serving to jeopardize these achievements.

Chile is a country that has implemented a successful housing sector reform program that has been fine-tuned over many years. Like Thailand, it reformed its government housing finance system in the 1980s. It introduced demand-side subsidies linked to market-rate loans for the middle income segment. Its private housing finance system expanded and so did the private housing market. Gradually, Chile was able to decrease the proportion of the population that cannot access market provided housing, but with increasing subsidy levels. It adjusted its approach to support housing for the lowest-income group many times, and, currently, supports the supply of housing for the poor with very high supply-side subsidies channeled through NGOs. The recent economic down-turn has put pressure on the subsidy budget, however. This cloud may have a silver lining. It may entice Chile’s housing ministry to analyze whether its liberal housing subsidy system may in fact have price effects that it should address.

Outstanding issues in both countries are the lack of development of a private rental sector.

Below is an iMFdirect post by Maurice Obstfeld, Gian Maria Milesi-Ferretti, and Rabah Arezki:

Oil prices have been persistently low for well over a year and a half now, but as the April 2016 World Economic Outlook will document, the widely anticipated “shot in the arm” for the global economy has yet to materialize. We argue that, paradoxically, global benefits from low prices will likely appear only after prices have recovered somewhat, and advanced economies have made more progress surmounting the current low interest rate environment.

Since June 2014 oil prices have dropped about 65 percent in U.S. dollar terms (about $70) as growth has progressively slowed across a broad range of countries. Even taking into account the 20 percent dollar appreciation during this period (in nominal effective terms), the decline in oil prices in local currency has been on average over $60. This outcome has puzzled many observers including us at the Fund, who had believed that oil-price declines would be a net plus for the world economy, obviously hurting exporters but delivering more-than-offsetting gains to importers. The key assumption behind that belief is a specific difference in saving behavior between oil importers and oil exporters: consumers in oil importing regions such as Europe have a higher marginal propensity to consume out of income than those in exporters such as Saudi Arabia.

World equity markets have clearly not subscribed to this theory. Over the past six months or more, equity markets have tended to fall when oil prices fall—not what we would expect if lower oil prices help the world economy on balance. Indeed, since August 2015 the simple correlation between equity and oil prices has not only been positive (Chart 1), it has doubled in comparison to an earlier period starting in August 2014 (though not to an unprecedented level).

Past episodes of sharp changes in oil prices have tended to have visible countercyclical effects—for example, slower world growth after big increases. Is this time different? Several factors affect the relation between oil prices and growth, but we will argue that a big difference from previous episodes is that many advanced economies have nominal interest rates at or near zero.

Supply versus demand

One obvious problem in predicting the effects of oil-price movements is that a fall in the world price can result either from an increase in global supply or a decrease in global demand. But in the latter case, we would expect to see exactly the same pattern as in recent quarters—falling prices accompanied by slowing global growth, with lower oil prices cushioning, but likely not reversing, the growth slowdown.

Slowing demand is no doubt part of the story, but the evidence suggests that increased supply is at least as important. More generally, oil supply has been strong owing to record high output from members of the Organization of the Petroleum Exporting Countries (OPEC) including, now, exports from Iran, as well as from some non-OPEC countries. In addition, the U.S. supply of shale oil initially proved surprisingly resilient in the face of lower prices. Chart 2 shows how OPEC output has recently continued to grow as prices have fallen, unlike in some previous cycles.

Continue reading here.

"By not reflecting liquidity risks in capital requirements, banking and insurance regulators have conjured up a dangerous system in which financial firms without liquidity take liquidity risks and financial firms with liquidity fail to do so. Two simple regulatory steps could change this system. Financial firms need to maintain a long-term stable funding ratio, and the regulatory risk weightings of assets should take into account the maturity of liabilities. These changes would encourage institutions with liquidity (life insurers, pension funds, and others with long-term liabilities) to provide it through instruments such as the self-rescheduling mortgage. They would also encourage banks to sell their illiquid assets to institutions with liquidity or lighten their dependency on short-term funding. The financial system as a whole would then be able to take long-term risks more safely. History suggests that safer housing finance would do more to make the financial system resilient than all the other recent initiatives put together", according to Avinash Persaud of the Peterson Institute for International Economics.

Via iMFdirect:

Canada’s housing market is sizzling hot and the Bank of Canada has a monetary policy dilemma: increase interest rates to cool the housing market would hurt borrowers and the economy; keep interest rates low adds fuel to the borrowing that led to the rise in housing prices and in household debt. What to do?

Housing headache

The latest national data on house prices in February suggest a year-on-year increase of 9 percent. House prices in Vancouver and Toronto—that contribute about a third of Canada’s GDP—have led the increase.

Canada’s housing boom has been accompanied by a steady rise in the nation’s household debt to 165 percent of disposable income by the end of 2015 (see chart). One way to cool the housing sector is to increase interest rates, but that would hurt the slowing economy, which has been hit hard by the decline in oil prices. Hence, the dilemma.

Low mortgage rates are an important factor feeding the housing market boom. This has helped keep interest payments low even as the size of the average mortgage has risen. As the figure shows, the share of interest payments in households’ disposable income has declined from 9 percent in 2008 to 6 percent in 2015, while the average size of mortgages has increased by some 40 percent over the same period. This means more households are able to afford more expensive homes, which, in turn, prompts households to borrow more money and get further into debt, while house prices continue to be pushed upward. This process should continue as long as employment is robust and interest rates remain low.

The Bank of Canada is rightly concerned about the rise in household debt, which makes the economy more vulnerable to unanticipated shocks and financial strains more probable. A mini version of this is playing out in Alberta, which has the third highest level of household debt among the provinces—after British Colombia and Ontario—and was hit by a large terms of trade shock from the oil price decline. The Alberta economy is expected to have contracted by almost 2 percent last year amid massive layoffs by the oil industry and house prices fell by 4 percent since their peak in late 2014.

Continue reading here.

"Should monetary policy use its short-term policy rate to stabilize the growth in household credit and housing prices with the aim of promoting financial stability? (…) the answer is no— especially when the economy is slowing down", according to a new IMF working paper by Andrea Pescatori and Stefan Laseen--Financial Stability and Interest-Rate Policy: A Quantitative Assessment of Costs and Benefits.

The paper notes that "At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices."

The paper's "findings show that it is very unlikely that the benefits of having a meaningfully tighter policy (i.e., at least 25 basis points higher than otherwise) would outweigh its costs, in the current Canadian context. In fact, even though the interest rate increase reduces the growth of real household credit and house prices and the ratio of household debt to GDP, the reduction in the crisis probability is minor and peaks only after about 8 years. At the same time, costs are front loaded and magnified by the tighter economic conditions. The policy rate path which takes into account financial stability risks is, thus, only 6 basis points higher than otherwise (for 8 quarters)—which, quantitatively, is not a meaningful policy alternative. A policy rate that is 25 basis points higher than otherwise (for 8 quarters) is expected to be welfare improving only under a scenario where a crisis would impose severe costs on the economy and real credit is expected to grow (in absence of policy intervention) at or above 9 percent a year for the next 3 consecutive years."

From Saurabh Mishra:

Structural transformation depends not only on how much countries export but also on what they export and with whom they trade. In my new IMF working paper with Rahul Anand and Kalpana Kochhar, we break new grounds in analyzing India’s exports by the technological content, quality, sophistication, and complexity of India’s export basket. The paper can be found here. Here are few key pieces of evidence from our paper:

Technological content of India’s exports

The evolution of Indian exports has not followed a “textbook” pattern. The pattern of evolution points to a dichotomy in the Indian economy – a well integrated, technologically advanced services sector and a relatively lagging manufacturing sector. The share of service exports in total exports has grown to over 32 percent in 2013 from 28 percent in 2000. On the other hand, the share of manufacturing exports in total export has declined to 67 percent from nearly 80 percent during 1990-2013.

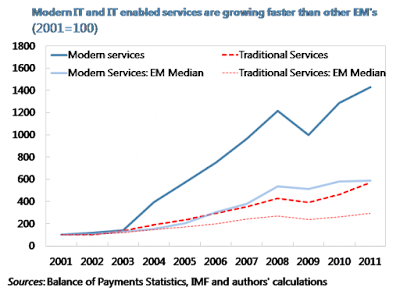

The growth in service exports has been more rapid, resulting in the share of services exports in total exports to increase rapidly over the last decade. This can be explained by technological changes. Many services do not require face-to-face interaction, and can be stored and traded digitally. These services are called modern services. Modern services are the fastest growing sector of the global economy. This is particularly evident in India, where modern services exports account for nearly 70 percent of the total commercial services exports (compared to around 35 percent in EMs) (see Figure 1).

Within manufacturing exports, there is a clear shift away from traditional exports, such as textiles, gems, and leather products, towards high-tech and medium-tech manufacturing products. The relative share of high-tech manufacturing exports has been increasing (however lower when compared to China or other EMs); Resource based production and low-tech manufacturing dominate the goods export basket (Figure 2).

Manufactured machinery accounts for almost 10 percent, while textile and garments account for more than 15 percent of India’s merchandise exports. In resource-based products – refined petroleum oil, cotton, jewelry of precious metals, and rice – constitute majority of export. In low-tech manufacturing exports – jewelry, textile and apparel based exports constitute the majority of India’s exports. In medium-tech manufacturing – the automotive industry dominates the basket, with machinery, various motor vehicle intermediary inputs for cars, bikes, construction, mining equipment and cosmetics making up the major portion. In the high technology export basket – veterinary and pharmaceutical products, television, telecommunication transistors, aircraft components, X-ray equipment and electronic R&D in electro-medical, power and automotive industry are key elements of the export basket. The main contribution of our work is to comprehensively document Indian exports, which has not been done over the past decade.

Continue reading here.

"Property prices have been subdued, in tandem with slowing economic growth and weak business sentiment", notes IMF's report on Indonesia.

"Property prices have continued to fall from their crisis peaks, in part because Russian buying has fallen", notes the IMF's report on Montenegro.

"After a long period of rapid growth, house prices have stabilized since 2013. A sharp reversal could have a significant impact on consumption, even if banks’ exposures could be managed (...). However, staff analysis does not suggest a major overvaluation, as past price trends were broadly in line with borrowing cost, demographic and income developments", according to the IMF's new report on Belgium.

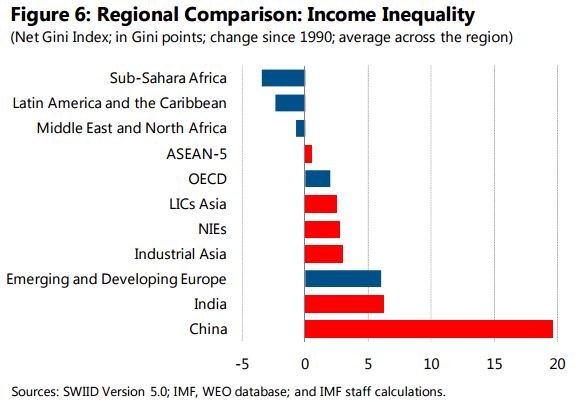

A new IMF "paper focuses on income inequality in Asia, its drivers and policies to combat it. It finds that income inequality has risen in most of Asia, in contrast to many regions. While in the past, rapid growth in Asia has come with equitable distribution of the gains, more recently fast-growing Asian economies have been unable to replicate the “growth with equity” miracle. There is a growing consensus that high levels of inequality can hamper the pace and sustainability of growth. The paper argues that policies could have a substantial effect on reversing the trend of rising inequality. It is imperative to address inequality of opportunities, in particular to broaden access to education, health, and financial services. Also fiscal policy could combat rising inequality, including by expanding and broadening the coverage of social spending, improving tax progressivity, and boosting compliance. Further efforts to promote financial inclusion, while maintaining financial stability, can help."

"Given still strong credit growth and rapidly rising house prices, the RBF should adopt macroprudential measures to tame the credit and housing price momentum, including through the use of loan-to-value ratios", says IMF report on Fiji.

"Housing markets have decelerated somewhat since mid-2014, but significant pressures remain. (...) Persistent upward pressure on house prices partly reflects supply constraints. (...) High house prices result in some households taking on high leverage, posing financial stability risks. (...) Further macroprudential tightening may thus be needed if the reduction in high leverage mortgages does not continue", says the IMF's new report on the United Kingdom.

A separate IMF paper examines how tax reforms could help ease structural supply constraints in the UK’s housing market. "Property taxation in the UK delivers larger revenue as a percent of GDP than any other OECD country. (...) However, a closer look at the UK’s property tax system suggests that some areas could be reformed to reduce constraints on housing supply and thereby reduce risks stemming from high house prices. In particular, deducing council tax discounts [and (...)] reducing reliance on the stamp duty land tax."

After countries remove restrictions on capital flows, inequality often gets worse

In June 1979, shortly after winning a landmark election, Margaret Thatcher eliminated restrictions on “the ability to move money in and out” of the United Kingdom, which some of her supporters regard as “one of her best and most revolutionary acts” (Heath, 2015).

Thatcher’s critics [have] regarded this same liberalization as starting a global trend whose “downside . . . proved to be painful” (Schiffrin, 2016). In their view, while the free mobility of capital across national borders confers many benefits in theory, in practice liberalization has often led to economic volatility and financial crisis. This in turn has adverse consequences for many in the economy, particularly for those who are not well off. Liberalization also affects the relative bargaining power of companies and workers (that is, of capital and labor, respectively, in the jargon of economists) because capital is generally able to move across national boundaries with greater ease than labor. The threat of being able to move production abroad reduces labor’s bargaining power and the share of the income pie that goes to workers.

In studying such distributional effects of capital account liberalization, Davide Furceri and I found that after countries take steps to open their capital account, an increase in inequality in incomes within countries follows (Furceri and Loungani, 2015). The impact is greater when liberalization is followed by a financial crisis and in countries where there is low financial development—that is, where financial institutions are small and access to these institutions is limited. We also find that the share of income going to labor declines in the aftermath of liberalization. Thus, like trade liberalization, capital account liberalization can lead to winners and losers. But while the distributional effects of trade have long been studied by economists, the distributional impacts of opening the capital account are just starting to be analyzed.

Read the rest of this (non-technical) summary of our results here: http://www.imf.org/external/pubs/ft/fandd/2016/03/furceri.htm

Here’s a link to the IMF Working Paper: http://www.imf.org/external/pubs/ft/wp/2015/wp15243.pdf

Earlier versions of this research, based on data for advanced economies, were featured on Krugman’s blog and in VoxEU. These new results extend our results to developing economies as well as lay out possible channels through which capital account liberalization leads to inequality.

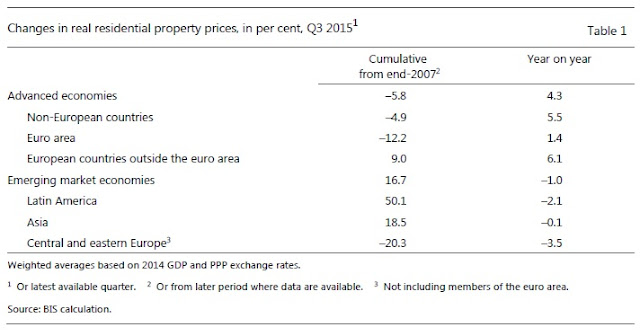

“Global house price boom accelerates further, led by Europe, North America, and some parts of Asia Pacific”, according to the Q3 2015 quarterly note from the Global Property Guide. This house price boom is reflected in two measures. First, real house prices rose in 28 out of a sample of 41 countries. Second, there is stronger upward momentum—in 22 countries house prices have risen faster compared to the previous quarter. These results are also in line with the Q3 2015 data reported by Knight Frank. Of the 55 housing markets tracked by Knight Frank, 82 percent recorded positive annual price growth, up from 75 percent. However, FITCH notes that even though the housing and mortgage outlook for the 22 countries remain stable/positive, divergence is increasing.

Looking at global house price developments in more detail, the Bank for International Settlement (BIS) says that real house prices increased by 4.3 percent year-on-year in advanced economies vs. a decline of 1.0 percent in emerging market economies. Within emerging market economies, the BIS notes that “there were significant disparities across countries: while prices continued to rise strongly in Hong Kong SAR, India and Turkey, they kept falling in Brazil, China and Russia.” Going forward, “the EM house price boom will be curbed by slowing income growth and weaker economic prospects”, says Oxford Analytica.

In the Euro area—where house price data coverage is higher compared to other regions—house prices rose by 2.3 percent in the third quarter of 2015 compared with the same quarter of the previous year, according to Eurostat. On the outlook for Europe, FITCH says that “Rising GDP, low rates, recovering credit flows, and improving labour markets will support the bounce-back in the eurozone periphery.” Moreover, according to Urban Land Institute’s Emerging Trends Europe, the five leading cities for investment prospects in 2016 are Berlin at Number 1, followed by Hamburg, Dublin, Madrid and Copenhagen.

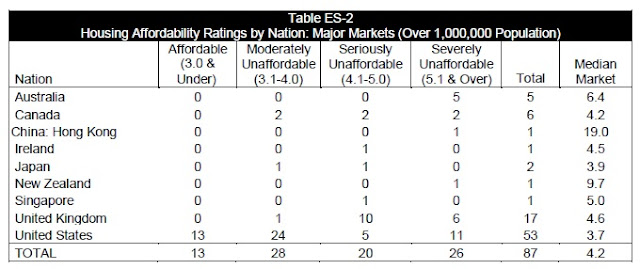

Finally, the latest survey from Demographia International Housing Affordability Survey finds that “The most affordable major metropolitan markets in 2015 were in the United States, which had a moderately unaffordable rating of 3.7, followed by Japan, with a Median Multiple of 3.9. Major metropolitan markets were rated "seriously unaffordable," in Canada (4.2), Ireland (4.5), the United Kingdom (4.6) and Singapore (5.0). The major markets of Australia (6.4), New Zealand (9.7) and Hong Kong (19.0) were severely unaffordable.”

A new IMF paper by Sami Ben Naceur and RuiXin Zhang "(...) provides evidence on the link between financial development and income distribution. Several dimensions of financial development are considered: financial access, efficiency, stability, and liberalization. Each aspect is represented by two indicators: one related to financial institutions, and the other to financial markets. Using a sample of 143 countries from 1961 to 2011, the paper finds that four of the five dimensions of financial development can significantly reduce income inequality and poverty, except financial liberalization, which tends to exacerbate them. Also, banking sector development tends to provide a more significant impact on changing income distribution than stock market development. Together, these findings are consistent with the view that macroeconomic stability and reforms that strengthen creditor rights, contract enforcement, and financial institution regulation are needed to ensure that financial development and liberalization fully support the reduction of poverty and income equality."

Here are some of my previous posts on capital account liberalization and inequality.

My presentation today at CIGI tries to provide a framework for the IMF's various recent policy forays and some of the key changes in IMF advice.

"House price growth was strong over recent years but has moderated recently", says IMF's report on Austria.

"The turnaround in house prices presents an opportunity to implement policies to better insulate Dutch households and the overall economy from the effect of future house price declines and remove some of the incentives for excessive leverage—thereby reducing the likelihood and intensity of boom-bust cycles", according to the IMF's report on the Netherlands.

Moreover, the report notes that "House prices have started to recover. However, they remain well below peak levels. Prices have risen by more than 5 percent since the 2013 trough, but they are still 17 percent below their 2008 peak in 2015:Q3. More than a quarter of Dutch households have mortgage debt in excess of the house value, primarily among younger households. The recovery in housing prices is uneven. The market is buoyant in Amsterdam, where house prices are less than 4 percent below the 2008 peak, and to a lesser extent in other major cities. However, house price increases are more subdued in outlying areas."

"House price inflation in Auckland has remained high. House prices in Auckland (where about one-third of the population lives) have continued their strong upward trend, rising by 22.5 percent (y/y) in December 2015, and the housing inventory available for sale remains low. Moreover, prices in neighboring areas are beginning to accelerate as buyers are priced out of the Auckland market. Supply shortages are a fundamental driver of house price inflation, exacerbated by high net immigration. On the demand side, macroprudential measures introduced in 2013 have led to a temporary slowdown in house price inflation. A package of additional macroprudential regulations and tax measures aimed at containing risks emanating from the Auckland housing market was announced in May 2015, but having become fully effective only in November, its effectiveness to cool rapid house price growth is yet to be seen", says IMF's new report on New Zealand.

A separate IMF paper "analyzes long-run trends in house prices and household debt in New Zealand. The key findings are that economic fundamentals such as financial liberalization, lower interest rates, demographics and supply constraints are important factors in the large run up in house prices. Although higher house price and household debt can largely be explained, it still has implications for financial stability."

"There is little evidence of a housing bubble, as the price increase over the past 10 years appears modest relative to nominal GDP growth", according to IMF's report on Morocco. The report also notes that "Several prudential tools have been used to manage systemic risk. A code of ethics was adopted by banks in 2008 to tighten lending standards for real estate. In addition, an increased tax on nonprimary housing was used to discourage speculative house purchases in 2006–08. Credit growth decreased from 24.4 percent in 2008 to 10.4 percent in 2009 (...)."

The 2016 Stekler Award for Courage in Forecasting goes to Michael ("Mish") Shedlock. At the start of 2015, the blogger popularly known as "Mish" had predicted recessions in Canada and the United States during 2015. While these events did not come to pass, enough anxiety was generated about the health of these economies over the course of the year that Mish deserves some credit for anticipating a degree of weakness that was not being widely talked about at the start of last year.

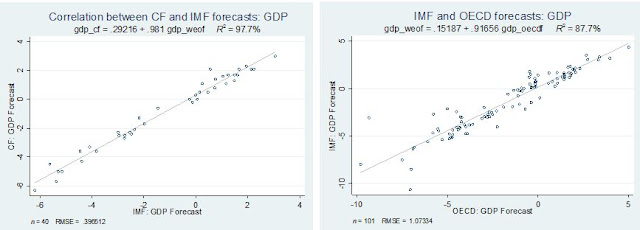

The Stekler Award is named after the famous forecasting expert and academic Herman Stekler who believes that recessions should be forecast "early and often." In practice, recessions are almost never forecast in advance. The Economist recently re-discovered this long-standing finding and highlighted the poor record of the IMF in forecasting recessions. The record of other public institutions or the private sector is just as poor. For instance, see the charts below on forecasts made by the IMF, OECD and the private sector (labeled ‘CF’ in the charts) over the course of 2009—each point shows the forecast for a particular country. The forecasts are virtually identical. And the forecasts for recessions (negative growth) were not made in advance by any of the sources.

The race is on for the 2017 award. Suggestions are welcome and can be sent to ploungani@gmail.com. The Stekler Award recognizes forecasts that depart significantly from the consensus view. Predictions need not be restricted to forecasts of recessions but they must be specific (so "oil prices will rebound someday" doesn't cut it) and well reasoned (so no "we have been on the path to doom which is bound to come one day"-type of forecasts).

We mined a recent article in Politico to see if we could get some front runners for the 2017 award. There were a range of predictions, some quite clever (Dean Baker predicted that during 2016, unlike 2015, oil prices would not fall another $60 a barrel), some specific (Ann Harrison predicts that "India will replace China as the leading destination for foreign investment" in 2016), most quite gloomy. On the U.S. economy in 2016, most experts surveyed stuck to the center, though Robert Reich said: "I expect the U.S. economy to sputter in 2016"; if he'd been a little more specific he 'coulda been a contender'.

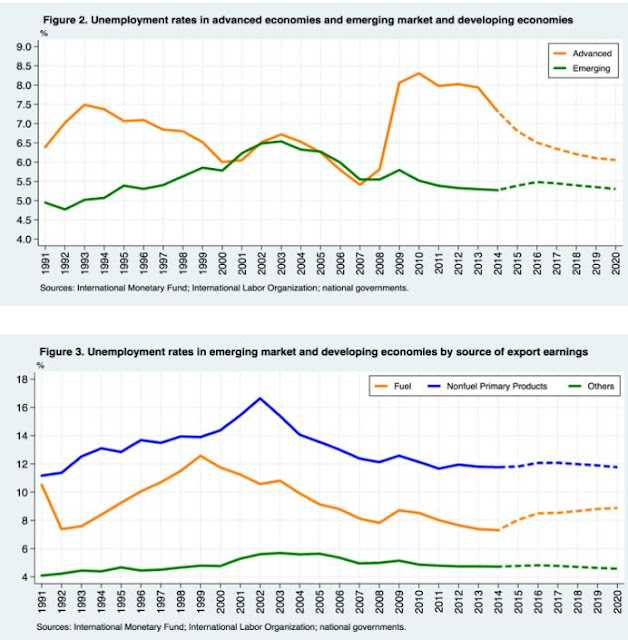

Figure 1 provides a measure of the global unemployment rate based on data for 116 countries, of which 37 countries are classified as ‘advanced’ (i.e. high-income) countries and the remaining 79 as ‘emerging market and developing economies.’ (We refer to the second group using the acronym ‘EMDE’.)

Let’s begin with how the global unemployment picture looked before the IMF’s January 2016 WEO Update. Figure 1 provides a measure of the global unemployment rate based on data for 116 countries, of which 37 countries are classified as ‘advanced’ (i.e. high-income) countries and the remaining 79 as ‘emerging market and developing economies.’ (We refer to the second group using the acronym ‘EMDE’.) Focusing on the recent cycle, global unemployment rate peaked in 6.2 percent in 2009 and has since been returning slowly to its pre-crisis level. Over the coming year, the global unemployment rate is expected to go up slightly.

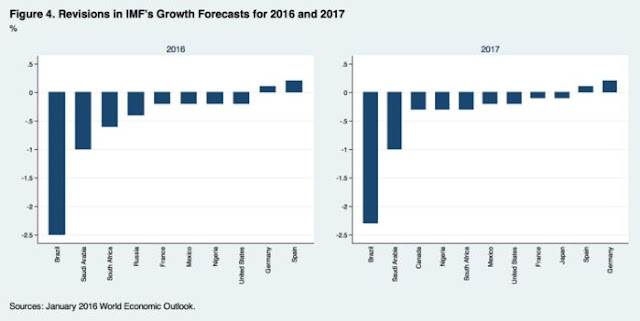

To understand where this increase is coming from, Figure 2 shows the unemployment rate for the two main groups of countries separately. This reveals that the increase comes from the emerging markets and developing countries (EMDE) group. Moreover, the increase in unemployment among this group occurs because of the expected increase in unemployment among fuelexporting countries (Figure 3).

How will the growth revisions affect the unemployment picture?

Now let’s consider how the revisions to the growth forecasts that the IMF announced in the January 2016 WEO Update could change the unemployment picture. At the global level, the forecast for GDP growth in 2016 was revised down by 0.2 percent, which would in turn increase the global unemployment rate only a little bit above the path projected in Figure 1. However, for some countries the revisions in growth forecasts are larger, as shown in Figure 4 below. The biggest change is in Brazil, followed by Saudi Arabia, South Africa and Russia.

Continue reading here.

The steady increase in China’s house prices at the national level masks tremendous variation at the city level, conference participants stressed in Shenzhen last month.

House prices in China have been on a long upward march over the past decade prompting questions about what the future holds (see Chart 1). At a conference last month in Shenzhen leading analysts of China’s housing markets provided some answers.

Organized by the IMF in cooperation with the Chinese University of Hong Kong, Shenzhen and Princeton University, the conference—International Symposium on Housing and Financial Stability in China—spotlighted new data sets on China’s housing markets, which provide informed views of what might happen next.

The conference was part of a series of conferences organized as part of the Global Housing Watch initiative, which also provides a quarterly update on conditions in housing markets. The latest update, released today, shows how China’s house price changes compare with those around the globe.

Demand-Supply Imbalances

Participants at the Shenzhen conference stressed that the steady increase in China’s house prices (see Chart 1) at the national level masks tremendous variation at the city level. Beijing has “experienced one of the greatest booms ever seen in housing markets,” according to real estate expert Joe Gyourko (University of Pennsylvania), but the situation is different elsewhere. With his co-authors, Gyourko has constructed a residential land price index for 35 large cities in China based on government sales of land to private developers. These data show that prices have increased in inflation-adjusted terms by about 80 percent a year in Beijing over the past decade but by only 10 percent a year in Xian (see Chart 2).

Continue reading here.

Kevin Drum--a political blogger for Mother Jones--asks: "But I wonder who did better at predicting recessions? Goldman Sachs? The CIA? A hedge fund rocket scientist in Connecticut? Whoever it is, it sounds like the IMF might want to look them up."

But as Drum noted in the Economist article, "Despite forecasters’ best efforts, growth is devilishly hard to predict".

Last year, in September, my presentation at the Federal Forecasters Conference summarized my work on the inability or unwillingness of forecasters to predict recessions. I suggested that to get forecasters to predict recessions (even inaccurately) we should have a Stekler Award for Courage in Forecasting. The award would be in honor of noted forecaster Herman Stekler who says that forecasters should predict recessions early and often and that he himself has predicted 9 of the last 5 recessions.

For my recent work on forecast accuracy see the following:

- September 2015: Fail Again? Fail Better? On the Inability to Forecast Recessions

- April 2014: “There will be growth in the spring”: How well do economists predict turning points?

Please bear in mind that this is intended to be a summary of views of external analysts and should not be attributed to the IMF.

“12 months of growing crisis”—that’s how the Guardian summarizes the housing market developments of 2015. This could partly explain the recent housing market measures announced by the UK government. However, experts doubt that these measures will have any effect. What follows is an attempt to answer four key questions about these developments:

- What are the new policies that the UK government announced?

- Will house price head north or south?

- What can be done?

- What are the likely implications?

1. What are the new policies that the UK government announced?The short answer: a series of measures to ease house prices and boost the housing supply.

The long answer: in November, the UK government announced three new policies for the housing market in its joint Spending Review and Autumn Statement. First: a new Help to Buy equity loan scheme for London will give buyers 40 percent of the home value from early 2016, as opposed to 20 percent. Second: help people get on the housing ladder through Help to Buy: Shared Ownership scheme. Third: from April 2016, people purchasing additional properties such as buy to let properties and second homes will pay an extra 3 percent in stamp duty. Moreover, in January, the House of Commons approved additional measures to boost housing construction.

2. Will house prices head north or south?

The short answer: north.

The long answer: “Government initiatives to support home ownership and build new houses will fail to have any real impact in 2016, with UK property prices expected to keep climbing”, according to a recent Financial Times survey. The survey asked 88 economists the following question: What effect are government policies likely to have on the housing supply and demand in 2016? How much will they contribute to likely changes in house prices?

The result of the survey is consistent with other data showing a similar upward trend in house prices. According to another survey, there is a pick-up in both activity and price expectations reflecting a rush to purchase Buy To Let properties ahead of the change in the Stamp Duty in April, according to Simon Rubinsohn at Royal Institution of Chartered Surveyors. Moreover, “The housing market has enjoyed some smooth sailing in the past year, with a steady 6.6% growth in house prices during 2015 (…) If the current speed of house price growth continues into 2016, the value of the average home may soon pass the £300,000 watermark, having reached £250,000 in December 2013”, according to LSL Property Services/Acadata. The latest numbers from Halifax, Knight Frank, and Office for National Statistics also points to an upward trend in house prices.

3. What can be done?

The short answer: it is complicated.

The long answer: on one hand, there seems to be a consensus among the experts that rising house prices is a concern and that there is not enough housing supply. On the other hand, there doesn’t seem to be any consensus on what the best way is to deal with rising house prices and expanding the supply of housing.

For example, experts have different views on how to address the housing supply problem. Martin Wolf of the Financial Times proposes that “The government must slay the sacred cows — the greenbelts around cities being the holiest of all.” In contrast, “Building an extra 100,000 houses a year would make hardly any difference to the upward trajectory of prices,” according to Gordon Gemmill of the University of Warwick. Oliver Jones of Fathom Consulting says: “(…) the problem in the UK is not a shortage of supply, but an excess of demand (…)”. The Economist says: “Building more houses is only part of the remedy for high prices (…) For one thing, Britain is bad at putting houses where they are most needed.” Melanie Baker and Jacob Nell of Morgan Stanley say that “There are so many government policies on housing that it is difficult to be confident about the net impact.”

The complexity of the housing supply debate can also be seen in the chart above. It comes from Neal Hudson, of Savills, and reveals a bizarre relationship. It says: “This chart has big implications. Everyone goes on about how Britain needs to build 250,000 or so houses each year to keep up with demand. The chart, of course, implies that unless you get housing transactions up, private builders won't get anywhere near that figure (the public sector build very little housing). Now, the big question is: why does this relationship exist? Economists don't really know. However, here is one suggestion (…) Housebuilders, (…) tend to target the price of new-build houses at the upper decile of the prices prevailing in the local property market (ie, at the top 10% of all the houses sold nearby in a given period of time). If that is true, then you would expect there (roughly) to be one house built for every ten sold.”